The United Republic of Tanzania

National Social Security Fund (NSSF)

We Build Your Future

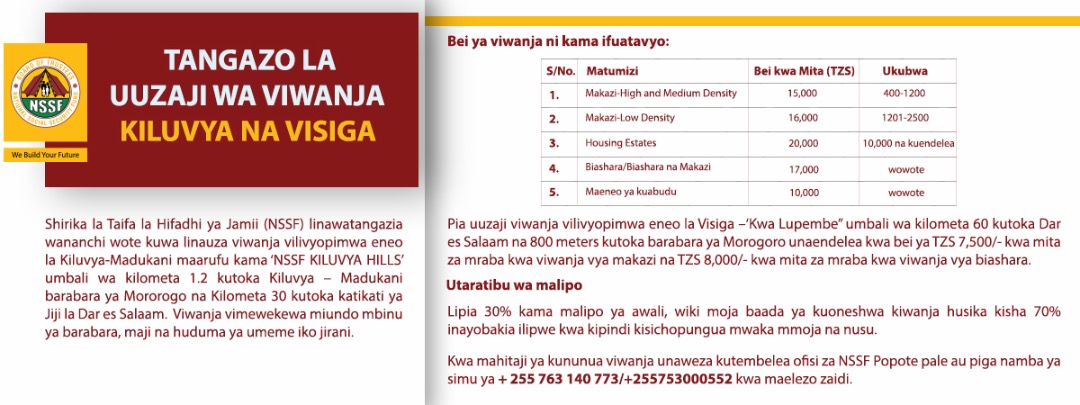

TANGAZO LA UUZAJI WA VIWANJA KILUVYA NA VISIGA

.

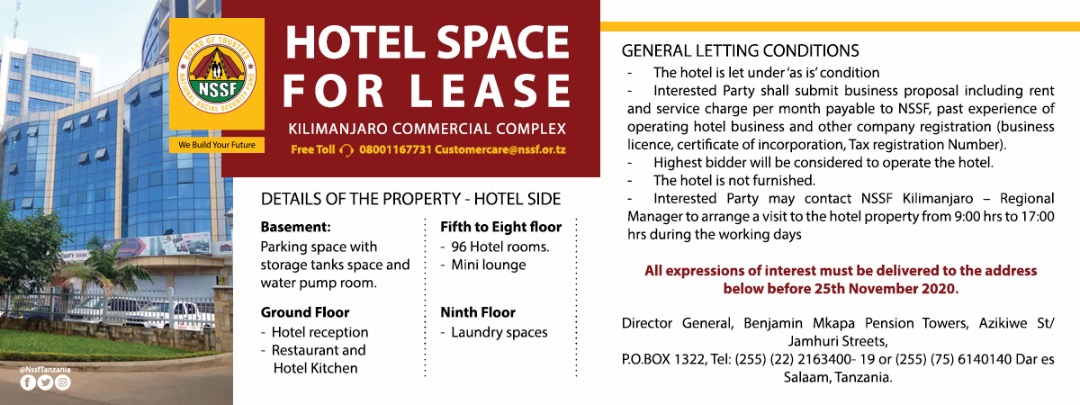

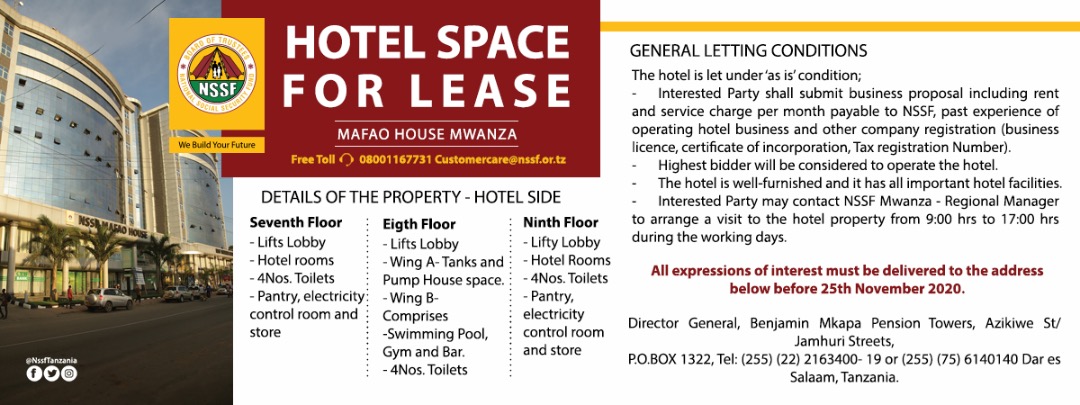

HOTEL SPACE FOR LEASE

.

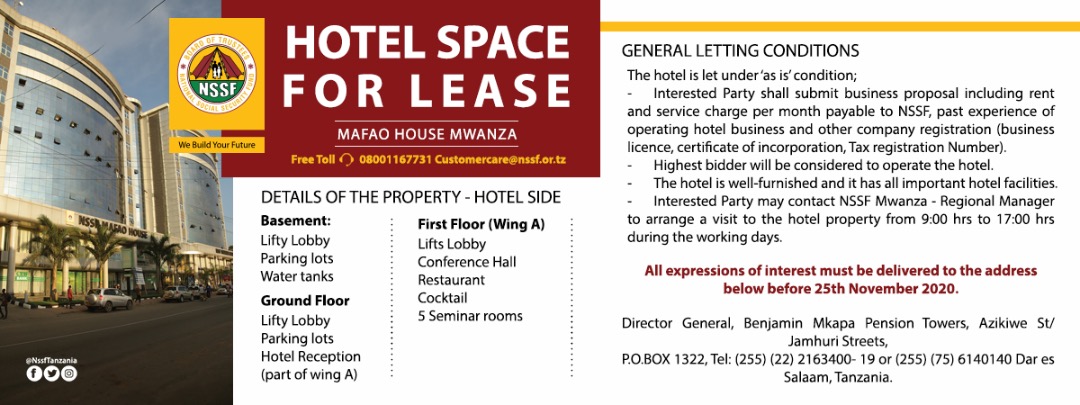

HOTEL SPACE FOR LEASE

.

HOTEL SPACE FOR LEASE

.

TOANGOMA Investment

TOANGOMA Investment

Kijichi Investment

Kijichi Investment

Dungu House

Dungu House

Kijichi Construction

Kijichi Construction

TOANGOMA House Investment

TOANGOMA House Investment

.jpeg)

.jpeg)